This summer Risk Salon is coming back for the 5th year. It is the NHC’s culture and belief to provide learning opportunities to everyone who is interested in the field. Registration for the event is entirely free. This event is hosted virtually via zoom meeting.

About Risk Salon

Risk Salon is a series of speaker events that brings in the industry veterans in the risk management field within the financial service sector. We have gathered the top insights, risk expertise from Toronto’s financial community to showcase in-depth knowledge and latest trends in risk management.

2021 Risk Salon – 4 Sessions

This year, we present four sessions on the following specific topics. Each session will be hosted on Wednesday evening (7:30PM).

Market Risk (FRTB) – August 11, 2021

Credit Risk – August 18, 2021

Emerging Risk: Climate Risk – August 25, 2021

Machine Learning in Finance – September 8, 2021

There will be presentations followed with a panel discussion when the audience are welcomed to comment and ask questions. Both risk management concepts and real risk problems faced by practitioners will be offered throughout each session. Both experienced elites and fledgling rookies will gain new knowledge from the class.

Event Information

Time: 7:30PM – 9:00PM

Date: August 11, 18, 25 and September 8, 2021

Sign up via eventbrite link or scan the QR code

Sign up for all four sessions or select the individual sessions you wish to attend.

Moderators and Guest Speakers List

This year, we are honoured to invite the following industry professionals as our panel moderator and guest speaker.

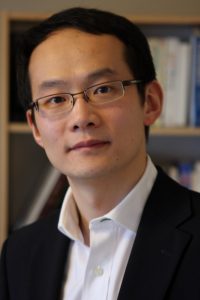

Dr. Dmitri Rubisov, Managing Director, BMO Capital Markets.

(Moderator)

Dr. Dmitri Rubisov has been with the Bank of Montreal since 2000, spent five years in risk management and later moved onto trading desk. He is now the head of Quantitative Strategies in BMO CM structured product desk.

Prior to that he was a post-doctoral fellow and research associate at the University of Toronto. He holds a Ph.D. degree in mathematical physics from Technical University of St. Petersburg. He has authored more than 30 papers with topics ranging from stability of motion, to process modelling, to chemical engineering and finally to pricing theory & statistics. As an Adjunct Professor at the Department of Statistical Sciences, University of Toronto, Dr. Rubisov has been teaching the Risk Management course as part of the MMF program for over 12 years.

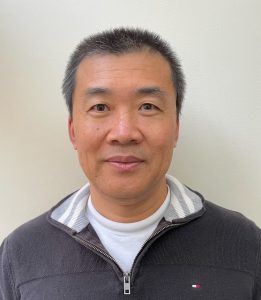

Dr. Jun Yuan, Managing Director and Head of CCAR Methodology, RBC

(Moderator & ML in Finance Session)

Dr. Jun Yuan is the Managing Director and Head of CCAR Methodology at RBC. He is also currently Adjunct Professor at the Rotman School of Management, University of Toronto (UoT). Jun holds a PhD in Electrical Engineering from UoT.

At RBC, Dr. Yuan is mainly responsible for leading the development, implementation and monitoring of risk models for market risk, counterparty credit risk and CCAR stress testing. Jun is a pioneer in applying machine learning and artificial intelligence techniques in financial innovation and risk management in capital markets.

Bin Li, Director, Market Risk Model Development, Scotiabank

(Market Risk Session)

Bin Li is a Director of Market Risk Model development team at Scotiabank. She is responsible for development, enhancement, and daily support for the current market risk capital models and the bank’s internal model approach for the FRTB project.

Bin has 16 years of financial industry experience in risk management with a wide range of skills, ranging from market risk and credit risk modelling, development, analytics and oversight, as well as regulatory initiatives and project management experience. Bin holds a Master of Science in Statistics from University of Toronto and a Bachelor of Engineering in Computer Science Software Engineering from Northeastern University in China.

Xiaofang Ma, Director, Market Risk Management, BMO

(Market Risk Session)

Xiaofang Ma is a Director of Risk Management at the Bank of Montreal (BMO). He has been leading the FRTB SA project from the Market Risk Models side since March 2021. He has about 15 years of quantitative model development experience, focusing on market risk and counterparty credit risk models. He has a PhD degree in Computer Science from the University of Toronto.

Shan Chen, Director, Risk Methodology (FRTB), RBC

(Market Risk Session)

Shan is currently a Director at RBC, covering risk methodology component of the Fundamental Review of the Trading Booking (FRTB) project at RBC. She has extensive experience in market and counterparty credit risk, with more than 10 years of working experience in various quantitative areas, including model validation and market risk methodology. She holds a Ph.D. in Economics from University of Waterloo and is a FRM charter holder.

Kewei Chen, Director, Counterparty Credit Risk, RBC

(Credit Risk Session)

Kewei is currently a Director in Counterparty Credit Risk at RBC. He worked in Local Market Risk covering Counterparty Risk Trading (CRT), FX, DCM and Corporate Treasury covering capital market liquidity over the last 4 years. Before RBC, Kewei held progressive roles in Scotiabank Group Treasury across various desks with focus on wholesale funding and liquidity.

Yan Cheng, Senior Director, Credit Model and Methodology, RBC

(Credit Risk Session)

Yan is currently a Senior Director in Credit Model and Methodology at Royal Bank of Canada (RBC). He was with market risk in the first 5 years covering equities, rates, and CVA. Since 2016, he moved to retail and enterprise credit modeling teams to build models for scorecard, allowance, and capital. Before RBC, Yan had led teams in derivatives structuring in Asia. He also taught financial engineering at City University of Hong Kong from 2008 to 2013.

In his spare time, Yan publish blogs on leadership and learning on https://teamyan.wordpress.com/

Alan Manning, Associate Director, Climate Risk Management, RBC

(Climate Risk Session)

Alan Manning is an Associate Director of Climate Risk Management at RBC. Over the past year, he has helped set up a new climate risk program for RBC’s UK subsidiary. Alan has focused on scenario analysis, both for physical and transition risks associated with climate change. Before that, he was in an enterprise risk rotational program, holding positions in market and operational risk. Alan joined RBC two and half years ago after completing a PhD in physics. When he’s not working he’s likely cooking, and he loves to meet new people and food from around the world.

Armando Benitez, Head of Quantitative Engineering (QE) and AI (DCT), BMO Capital Markets.

(ML in Finance Session)

Armando Benitez is the Head of Quantitative Engineering (QE) and AI (DCT) at BMO Capital Markets. QE & DCT is a group Engineers and AI Experts that delivers practical solutions at scale with a focus on revenue generation.

Armando joined the ETF desk at BMO Capital Markets in 2016. Prior to joining BMO, Armando built data products for Fraud Detection and Recommender Systems at Paytm. Armando obtained his Ph.D. in High Energy Physics performing data-intensive analyses at the Large Hadron Collider at CERN and Fermilab.

Jason Tuo, Risk Analytics & Solution Leader (FSRM), EY

(ML in Finance Session)

Jason Tuo is part of the Financial Services Risk Management Advisory (FSRM) practice at Ernst & Young (EY). He is leading the development of EY’s trusted AI framework and AI/ML validation standards which is unique in the market and a key differentiator.

Jason has over 15 years of experience in the financial services industry, covering credit risk modelling, risk analytics, capital management, risk strategy, Basel compliance, stress testing, RWA optimization and risk appetite. He focuses primarily on the development and validation of models for credit, market, counterparty credit and operational risk. He has led teams in numerous Basel and IFRS-9 regulatory transformation projects, both at industry and for his consulting clients.

Special Thanks to Dmitri and Jun!

Our special thanks go to Dr. Dmitri Rubisov and Dr. Jun Yuan who have made enormous efforts organizing this year’s risk salon series and inviting guest speakers. Both of them will be the moderators at panel discussions.